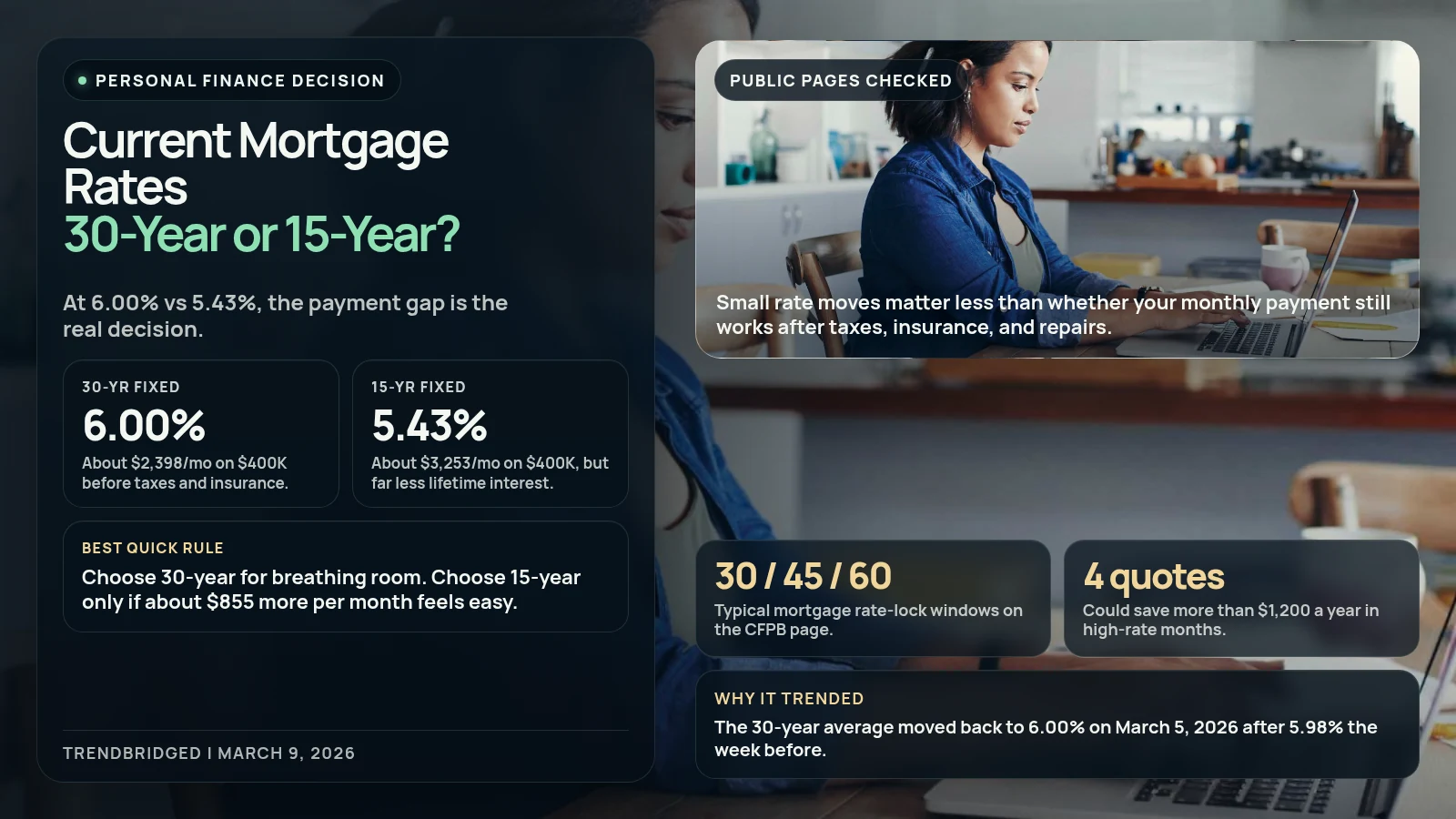

A mortgage decision feels different when the benchmark is sitting on the line. This guide answers one specific question: at current mortgage rates, should you choose a 30-year fixed mortgage or a 15-year fixed mortgage? On March 9, 2026, the lower-regret answer for most buyers is the 30-year unless an extra $855 per month on a $400,000 loan feels comfortable enough that you would gladly trade it for about $278,000 less interest over the life of the loan.

That conclusion is based on official materials and first-hand observation of the public Freddie Mac mortgage-rate pages and CFPB mortgage guidance checked on March 9, 2026. Search interest makes sense right now because Freddie Mac's weekly benchmark moved from 5.98% to 6.00% for the 30-year average between February 26 and March 5, 2026, while the 15-year average eased to 5.43%. When the 30-year is sitting right at 6%, the practical question is not whether rates are headline-friendly. It is whether your cash flow favors flexibility or faster payoff.

What Do Current Mortgage Rates Mean for a $400,000 Loan?

Start with the part that changes the decision fastest: the payment shape.

Using Freddie Mac's March 5, 2026 benchmark averages and standard principal-and-interest amortization math, the split looks like this:

| Option | Freddie Mac average rate | Monthly principal and interest* | Total interest over full term* | Payoff horizon |

|---|---|---|---|---|

| 30-year fixed | 6.00% | $2,398 | $463,353 | 30 years |

| 15-year fixed | 5.43% | $3,253 | $185,629 | 15 years |

* Our calculation on a $400,000 loan principal. Taxes, insurance, HOA dues, and mortgage insurance are not included.

That creates the real decision block:

- The

15-yearcosts about $855 more each month. - The

15-yearsaves about $277,724 in total interest if you keep the loan for the full term. - The

30-yearpreserves the most monthly flexibility even though its rate is only 0.57 percentage points higher.

That is why the lower rate on a 15-year can still be the wrong answer. The monthly payment jump is large enough that it matters more than the headline rate spread.

Is a 15-Year Mortgage Worth the Higher Payment Right Now?

Only if you can afford it without turning your budget brittle.

The official Freddie Mac pages make the top-line case for the 15-year obvious: the current average is 5.43%, below the 6.00% 30-year benchmark. But the more useful way to read that gap is not "the 15-year is cheaper." It is "the 15-year is cheaper in interest, but far more demanding in monthly cash flow."

Choose the 15-year if most of these are true:

- your emergency fund would still look healthy after absorbing roughly $855 more per month on the loan example above

- you expect to keep the home long enough for the lower total interest to matter

- you want a forced-paydown structure because you would not reliably prepay a 30-year on your own

- the higher payment still leaves room for taxes, insurance, repairs, and normal life volatility

Choose the 30-year if most of these are true:

- you want the lowest required payment, even if you plan to prepay when cash flow is strong

- you are buying near the top of your comfortable budget already

- you may move, refinance, or redirect cash toward renovations, childcare, or retirement accounts before year 15

- you do not want your mortgage decision to depend on a best-case income path

The short version is simple: pick the 15-year for balance-sheet efficiency, and pick the 30-year for budget resilience.

When Should You Lock a Mortgage Rate at These Levels?

This is where current mortgage rates stop being abstract.

The CFPB's rate-lock explainer says a mortgage rate lock means your interest rate will not change between the offer and closing as long as you close within the stated time frame and nothing important changes in your application. The agency also says rate locks are typically available for 30, 45, or 60 days, and that a lock can become expensive to extend if your closing slips.

That leads to a cleaner rule than trying to predict the next headline move:

Lockif your purchase is real, your closing is inside the lender's lock window, and the payment already fits your budget.Floatonly if your timeline is still loose enough that paying for or extending a lock would create more friction than benefit.

For this topic, the trend signal itself points the same way. Freddie Mac's weekly average only moved 2 basis points higher from the prior week. That is a reminder that small market moves matter much less than whether you are exposed to a sudden repricing while your deal is still open.

What Should You Compare Besides the Headline Rate?

A lot.

The CFPB's Loan Estimate guidance is more practical than most rate commentary. The agency says lenders must send a Loan Estimate within three business days after you submit the required information, and it advises borrowers to ask each lender for the same kind of loan with the same features so the comparison is clean.

That matters because a mortgage decision is not just 6.00% versus 5.43%. It is also:

- whether the rate is actually locked

- whether points or lender credits changed the quote

- whether risky features are hiding in the offer

- whether taxes and insurance estimates are realistic for the property

Freddie Mac's own research strengthens that point. In high-rate months, the company found that borrowers who got two rate quotes could save as much as $600 annually, while borrowers who got at least four quotes could save more than $1,200 annually.

So the better move is not to refresh rate trackers all day. It is to request multiple Loan Estimates fast enough that you can compare real offers while the same market conditions still apply.

What the Official Pages Actually Show Right Now

After checking the public Freddie Mac and CFPB pages on March 9, 2026, these are the most decision-useful facts:

- Freddie Mac's current public benchmark page shows March 5, 2026 averages of 6.00% for 30-year fixed and 5.43% for 15-year fixed.

- Freddie Mac's archive page shows the prior week's 30-year average at 5.98%, which helps explain why search interest spiked again when the line moved back to 6.00%.

- CFPB says a rate lock can still break if key parts of your application change, such as the loan amount, documented income, or credit profile.

- CFPB also says multiple mortgage credit pulls inside a 45-day window are recorded as a single inquiry for credit-report purposes.

That last point matters more than many borrowers think. If you are hesitating to compare lenders because you assume every extra quote will hurt your credit separately, the official guidance says the effect is treated as one inquiry inside that mortgage-shopping window.

Who Fits the 30-Year Better, and Who Fits the 15-Year Better?

Use this direct-answer block if you want the shortest possible recommendation:

Choose 30-yearif monthly breathing room matters more than finishing the mortgage fast.Choose 15-yearif you can absorb roughly $855 more per month on a $400,000 example without stressing the rest of your budget.Lock soonif closing is near and the payment already works.Shop more lendersif your decision is close, because official Freddie Mac research suggests extra quotes can still create meaningful savings in higher-rate environments.

This is also where discipline matters. If taking the 30-year would tempt you to spend the monthly difference instead of saving or prepaying, the 15-year can be the better forced structure. If taking the 15-year would make every repair, tax bill, or job wobble feel dangerous, the 30-year is the smarter fit even if the spreadsheet says otherwise.

If you are auditing monthly costs beyond housing, Costco Gas Prices: Is a Membership Worth It or Should You Use a Nearby Station? is the smaller recurring-expense version of the same decision: when does the lower headline price actually survive fees and friction? The broader Personal Finance hub collects more of these practical money choices.

Verdict

Current mortgage rates make the 30-year fixed the better default for most buyers, and the 15-year fixed the better fit for buyers with real payment room.

At Freddie Mac's current benchmarks, the 15-year is not winning because the rate is dramatically lower. It wins only if you want to trade $855 more per month for a much faster payoff and roughly $278,000 less interest on a $400,000 principal example.

So if your budget still feels tight after taxes, insurance, and the rest of homeownership, take the 30-year and keep flexibility. If your cash flow is strong and stable enough that the higher payment barely changes your day-to-day decisions, the 15-year is the cleaner long-term value play.